Regulating Financial Exchanges

Instead of stifling innovation, the federal government would simply provide the ethical boundary lines.

As I am the discoverer of human economies outside of Earth, reader of 460+ books, career work on Earth professionally in market data, web hosting, Ron Paul political campaigns, farming, and deep thought for 16 years how to improve Earth systematically, I believe that exchanges such as CME Group (USA), Shanghai Futures (China), and all others can achieve superior markets by bringing the regulation of fraud and violence on digital order books in house with their own legal teams. For example, this would remove the need for onerous, expensive court systems and SEC type agencies which hamper innovation.

Let us use CME Group Exchanges (CME, CBOT, NYMEX, and COMEX) as the case study for this article.

{kind=link}

History of government finance regulation in USA

The era in USA of pure self regulation for financial exchanges ended after the great depression. Before the great depression, NYSE and similar exchanges operated as clubs with their own rules. Everyone and their grandmothers were trying to figure out how prices collapsed on the biggest USA stock exchange, NYSE.

Securities Act of 1933 & Exchange Act of 1934 (1933-1934)

The 1933 Act (initially enforced by the FTC) forced companies to tell the truth about the securities they were selling. The 1934 Act created the SEC to police the secondary markets and officially ended the era of exchanges operating purely as private clubs.

The Maloney Act 1938

This amended the 1934 Act to allow the creation of the NASD. Congress realized the SEC didn't have the manpower to police thousands of over-the-counter brokers directly, so they deputized the industry to self-regulate under SEC supervision.

Creation of the CFTC 1974

As derivatives and futures trading exploded beyond traditional agricultural products, Congress created the Commodity Futures Trading Commission. Unlike the SEC, the CFTC is largely funded by congressional appropriations (taxpayer money), making it one of the few purely tax-funded market regulators.

Sarbanes-Oxley Act 2002

Following the Enron and WorldCom accounting scandals, the government stepped in to regulate the auditors. It created the PCAOB (Public Company Accounting Oversight Board) to oversee the accounting industry, effectively ending self-regulation for corporate auditors.

Creation of FINRA 2007

The NASD and NYSE Regulation merged to form FINRA. By the 2000s, having two different SROs with overlapping and sometimes conflicting rulebooks had become inefficient for Wall Street firms that were members of both. FINRA remains a private, industry-funded SRO.

Dodd-Frank Act 2010

The 2008 financial crisis exposed massive regulatory blind spots, particularly in the banking and swap markets. Dodd-Frank created the Consumer Financial Protection Bureau (CFPB) and the Financial Stability Oversight Council (FSOC) to monitor systemic risk across the entire financial system.

These regulations have piled up hampering innovation and burdening regulatory compliance teams at every broker-dealer in the world on CME Group exchanges. While some components of each action above are ethical and beneficial, a much better system is possible.

Stifling CME Group Innovation

Often, CME Group works to innovate regulations, new market connections, broker-dealer market data feeds, international agreements, rule-based litigation. Almost every time, they are met with fierce resistance from the SEC, the CFTC, or similar agencies in the USA and international jurisdictions. The United States of America has the best market systems overall, judging by market capitalization, data feeds, liquidity, and diverse financial instruments. This is often the source of confusion when analyzing US financial regulations; market participants assume that because the country has such a deep history of financial regulation, everything is running smoothly. Many advanced financial professionals disagree.

Example of systemic innovation for market data feeds

Personal experience gained while working at a high-frequency trading broker-dealer, Blue Fire Capital, and a market data feed company, Activ Financial, led me to an intense study on how to improve regulatory systems and data feeds.

The article above is one example of a change that could be made to make markets more efficient. The Utopia Educators text above explores how a new variable can be included in data feed networks to identify participants in real time, globally.

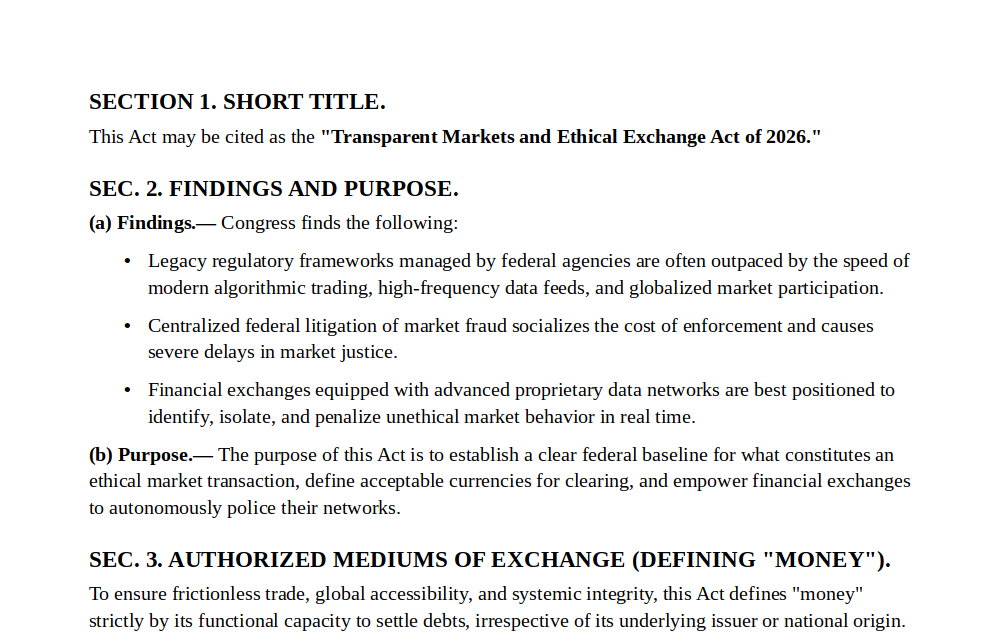

Example of ethical law at the federal level

To replace the labyrinth of outdated agency regulations, a federal ethical law could be established around a single, foundational USA federal act: Transparent Markets and Ethical Exchange Act of 2026.

Rather than dictating the exact technical specifications of every trade, data feed, or broker-dealer connection—rules which inevitably fall behind technological advancements—this federal mandate would establish a clear, unyielding ethical baseline. By defining ethical money and defining deceptive market practices, such as spoofing, wash trading, or deliberate latency arbitrage, without micromanaging the underlying software. The enforcement mechanism would then be decentralized to the exchanges themselves, such as the CME Group Exchanges.

Leveraging the advanced data feeds and real-time global participant identifiers explored earlier in this article, ultimately, this act would transform the CME Group into an autonomous, real-time regulatory body, empowered to instantly police and penalize bad actors using its own modern data systems.

By shifting to a principle-based federal law, we remove the multi-year lag associated with outsourced SEC or CFTC investigations and the costs of policing the market become a market vector for each exchange. The exchanges would then be able to build global market reputation, innovate profitable enforcement, create new jobs, and remove the need for constant litigation.

Instead of stifling innovation, the federal government would simply provide the ethical boundary lines. The exchanges—whose very survival and profitability depend on their market reputation, speed, and liquidity of their order books –would be fully empowered to police their networks in real time. The Transparent Markets and Ethical Exchange Act of 2026 law aligns the moral mandate of the legal system with the supreme technological capabilities of modern data systems and modern money systems, which ultimately foster a faster, safer, and highly efficient financial ecosystem.